Japan’s currency is pressuring the Bank of Japan to deliver its most significant rate increase in decades while edging closer to levels that have previously triggered historic foreign-exchange intervention.

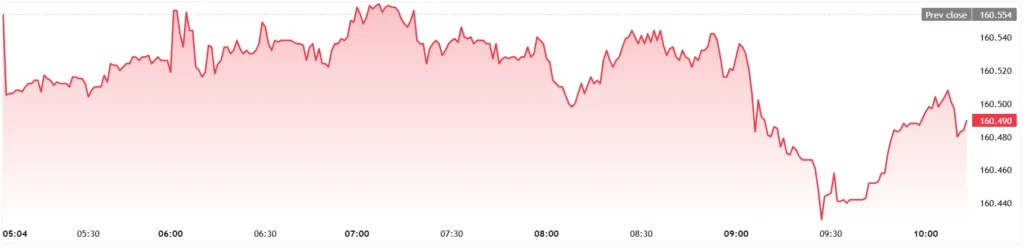

The yen weakened to around 160.5 against the US dollar on June 10, its highest since July 2024, even as traders priced in a likely quarter-point hike at the BOJ’s policy meeting ending June 16.

Officials have signalled that further tightening is feasible, with reports that officials are considering taking the benchmark rate to 1 percent and keeping the door open for additional moves later in the year.

Currency weakness defies prior intervention

The bears have been persistent. The yen underperformed all Group-of-10 peers in May despite record-scale intervention by Tokyo aimed at supporting the currency.

That resistance to intervention has raised the risk that the dollar could test or breach 160 yen well before any lift from higher Japanese rates arrives, according to market strategists.

Japanese authorities last intervened in the forex market in July 2024, when the yen slipped to a 30-year low near 162 against the dollar.

Policy normalization after years of ultra-loose easing

The BOJ has been winding down an unprecedented era of negative rates and yield controls that lasted more than a decade.

In December 2025, the central bank raised its short-term policy rate to 0.75 percent, the highest since 1995, marking a decisive step in policy normalization.

Markets have largely priced in another hike at the June meeting, with some analysts expecting the rate to reach 1 percent as officials weigh persistent inflation risks and still-low real rates.

Intervention threshold and market expectations

Finance Ministry officials have repeatedly warned against “excessive volatility” and unidirectional moves in the currency, without specifying exact levels for action.

Analysts at several banks have pointed to around 160 yen per dollar as a key reference point where intervention could become more likely, citing the need to avoid chaotic market dynamics.

The ministry operates under a September 2025 framework agreed with the United States, which allows for coordinated action if exchange rates move sharply and disrupt financial stability.

Wider implications for global markets

A stronger BOJ stance would narrow the rate differential with the US Federal Reserve, which has held rates higher for longer, potentially reducing the carry appeal of selling the yen.

However, if the yen remains weak despite intervention and a rate rise, doubts could grow about the durability of the BOJ’s tightening cycle, especially given concerns that higher policy rates may push up long-term government bond yields excessively.

Global markets are also watching how the BOJ calibrates tightening amid fiscal risks and rising public debt servicing costs, which could limit how aggressively policy can be normalized.

What could happen next

Investors will focus on the June 16 BOJ statement for guidance on the pace of future hikes, as well as any updated forecasts for growth, inflation and the exchange rate.

If the yen continues to hover near 160, the Ministry of Finance could again issue stronger warnings or act directly in the market, increasing short-term volatility in Asian trading sessions and potentially rippling into bond and equity markets across the region.

Financial markets will also be alert to how the US dollar reacts to the interplay between BOJ tightening and the US interest-rate outlook, given the outsized role of the dollar-yen pair in global risk sentiment and funding conditions.