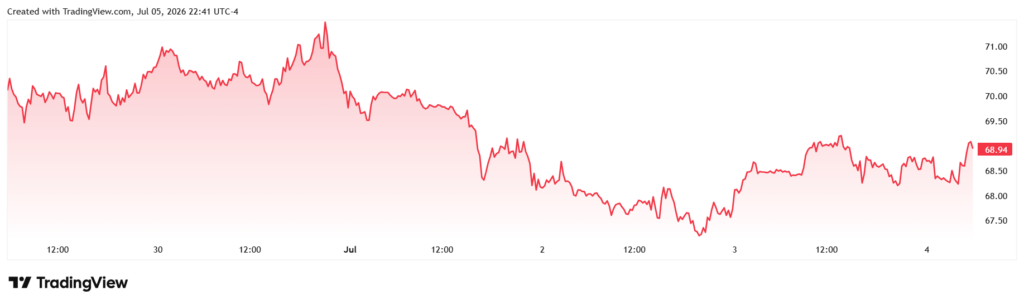

Oil prices edged lower on Monday after seven OPEC+ producers agreed to raise August production targets by 188,000 barrels per day, a fifth monthly increase that pushed traders back towards oversupply risk as Gulf exports recover.

By 0121 GMT, US West Texas Intermediate crude futures (CL) were down 0.5% at $68.78 a barrel. Brent crude futures (LCO) fell 0.2% to $71.96.

Market Snapshot

The move extended a retreat in crude that has followed the unwinding of a geopolitical premium built during the Iran conflict and disruptions around the Strait of Hormuz.

The Brent futures curve has stayed in contango, with nearer contracts priced below later delivery months. ANZ analysts described it in Monday commentary as a “bearish contango structure”, saying the shape pointed to expectations of looser prompt supply.

OPEC+ Decision

Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria and Oman agreed after a virtual meeting on Sunday to add 188,000 barrels per day from August. The increase extends a staged rollback of voluntary curbs first introduced in 2023 to support the market.

The group has raised targets for five consecutive months, but actual supply gains depend on field capacity, export routes and compliance. Producers are trying to restore barrels without accelerating a price slide that would squeeze revenues.

The next meeting is scheduled for 2 August, when the group is expected to review September policy.

Supply And Shipping

The decision landed as exports through the Strait of Hormuz, a key route for Gulf energy shipments, continued to recover. Saudi Arabia has restored exports to near pre-conflict levels, while other Gulf producers have increased output and shipments.

ANZ analysts said OPEC production rose by 2.34 million barrels per day in June as exports through the Strait of Hormuz resumed. They also warned that “ongoing risks to their vessels” could limit the extent to which added capacity reaches the market.

Security costs, insurance premiums and vessel availability remain important for physical flows. Any fresh disruption around Hormuz or the Red Sea could quickly rebuild risk premiums, especially for Asian buyers reliant on Gulf crude.

Demand Signals

The supply story has overtaken pockets of demand optimism. Lower Chinese crude imports have added to concerns that the market may move into surplus in the second half of 2026, particularly if OPEC+ barrels arrive while refinery demand softens.

China remains the largest global crude importer, making its purchasing patterns a key guide for traders. Weaker intake can reflect refinery maintenance, high inventories or softer fuel demand, but the effect is usually the same for futures: fewer immediate signs of tightness.

Official selling prices from Saudi Arabia and other Gulf exporters are therefore likely to draw close scrutiny. Lower prices for Asia would point to weaker demand or competition for market share, while firmer prices could indicate that refiners are still bidding for term supply.

Broader Context

For importing economies, lower crude can reduce fuel costs and ease inflation pressure after months of geopolitical volatility. For producers, a sustained fall would complicate budgets and could test OPEC+ unity, especially if members compete to regain volumes.

The latest increase also comes as traders reassess the value of geopolitical hedges. During the conflict, supply risk dominated pricing. As flows normalise, the market is returning to inventories, refinery runs, Chinese demand and the pace of non-OPEC supply growth.

Outlook

Traders will watch whether the August OPEC+ increase translates into real barrels, whether Hormuz flows continue to improve, and whether Chinese imports rebound after recent weakness.

The next signals will come from Gulf official selling prices, weekly inventory data and any shipping or security incidents that could alter the balance between recovering supply and still-fragile demand.