The pound (GBPUSD) hovered near 1.3205 in early London trade on Friday, stuck below the 1.33 handle as the Bank of England faces a sharpening policy dilemma between sticky inflation and growth risks from the Middle East oil crisis. Sterling has shed more than 650 pips from January’s peak near 1.3870, with Thursday’s 0.65% drop extending losses into a fourth straight session.

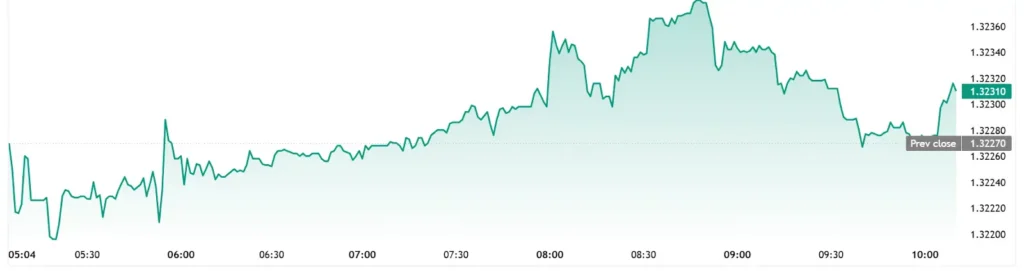

GBP/USD 1 Day Chart

Market Snapshot

GBP/USD (GBPUSD) traded at 1.3205 as of 10:00 a.m. London, down 0.12% on the day after testing 1.3180 support overnight. The pair faces immediate resistance at 1.3380-1.3399, with a break above needed to halt the downward momentum toward 1.3000. Against the euro, sterling slipped 0.40% to 85.59 pence (EURGBP 0.8559), while GBP/JPY fell 0.31% to 209.98 as risk-off flows favored the yen.

UK gilt yields retreated from recent highs but posted their sharpest monthly climb in over a year, with the 10-year (GB10YT=RR) up 6 bps on the day at 4.87% as investors priced in prolonged policy uncertainty.

Policy Conundrum

The BoE’s March 19 decision to hold rates at 3.75% left markets split on the next move, with money markets now pricing a 50% chance of a hike by April 30 rather than the cut previously expected. Inflation held steady at 3.0% year-on-year in February, double the central bank’s 2% target, while services inflation remains elevated at 5.2%.

“Markets have completely repriced from two cuts to two hikes in 2026, but the BoE has set a very high bar for moving rates higher,” said a London-based FX strategist at a major bank, speaking on condition of anonymity. “Until we see clear evidence that oil-driven inflation is feeding into wages, the committee will likely pause.”

BoE policymaker Alan Taylor struck a cautious tone last week, emphasizing that borrowing costs should remain steady until the economic impact of the Iran conflict becomes clearer. The central bank faces a stagflationary trap: Brent crude (LCOc1) surged above $107 a barrel on Friday, up 1.5% on the day, threatening to push UK inflation toward 4% in coming months while dampening growth.

Macro Implications

The oil shock has forced a stark reversal in BoE expectations. Traders had priced in two 25-basis-point cuts for 2026 as recently as early March. Now, at least two hikes are anticipated, with a third possible if Brent sustains above $105. This divergence with the Federal Reserve, which held rates at 3.75% in March but signaled a slower pace of disinflation, has widened the policy gap supporting the dollar.

“The stagflationary mix is toxic for sterling,” said a rates trader at a European bank. “The BoE can’t cut with inflation at 3% and oil at $107, but hiking into a growth slowdown risks a deeper downturn.”