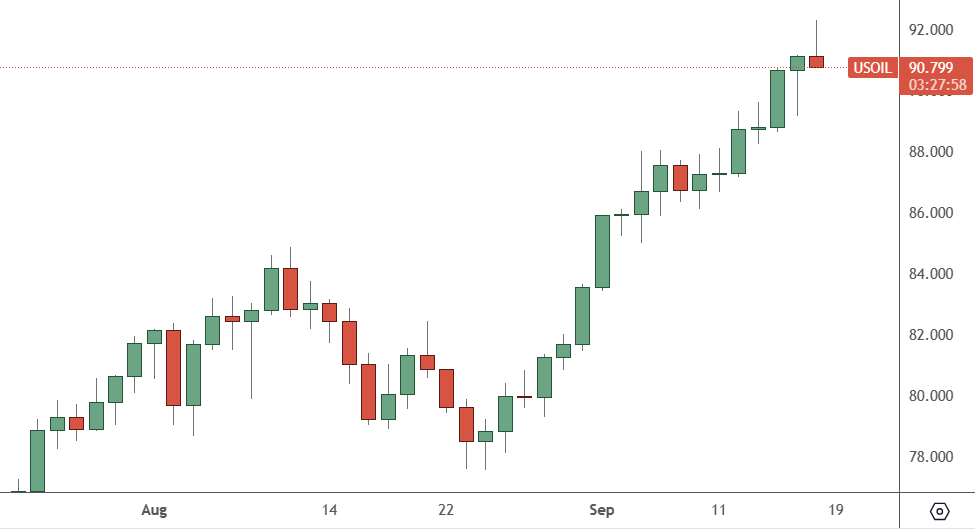

Oil prices showed some selling after a push to $92, and traders may be taking a pause in bullish activity at this level.

USOil: Daily Chart

Oil prices pushed higher again last week to get above the $90 level. The price has support on the daily chart at around $87 per barrel.

Saudi Arabia’s energy minister defended the latest decision to extend production cuts, saying the “jury is still out” on a global economic recovery.

Ironically, the surge in oil prices is a key factor in that shaky recovery. Riyadh and Moscow announced earlier this month that they would extend production cuts to the end of the year, pushing crude prices to 10-month highs.

Prince Abdulaziz bin Salman, the Saudi energy minister, told oil and gas industry leaders in Calgary that the decision was not “jacking up prices” but rather “making the decisions that are right when we have the data”.

Market analyst Ed Yardeni has now raised the odds of a recession in the US before the end of 2024, citing higher oil prices and widening deficits. In July, Yardeni lowered the likelihood of a recession, but the 30% spike in oil since late June has changed that.

“Today, in response to several new developments, we are raising the odds of a recession before the end of next year from 15% to 25%,” he wrote on Monday.

The current correction in oil on Monday may just be a short-term pause, with the support lying at $87. The United States will also have to decide on its SPR oil reserves, which were depleted after President Biden sold 180 million barrels from the stockpile. Saudi Arabia was angered last year that the US was not going to be topping up the reserves due to maintenance, and they missed out on prices at $65-70, which may be a mistake if oil pushes above $100 again.