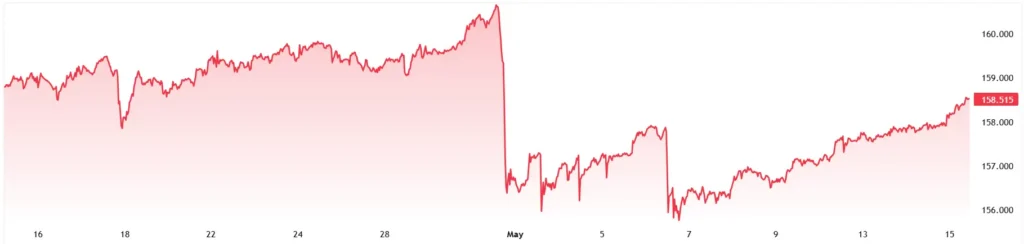

The dollar strengthened against the yen on Friday, with USD/JPY advancing toward 158.30, its highest level in nearly two weeks, as robust US economic data and rising Treasury yields reinforced expectations that the Federal Reserve will maintain a restrictive policy stance.

US retail sales rose 0.5% in April, matching economist forecasts and following a downwardly revised 1.6% gain in March.

The data underscored continued consumer resilience despite elevated borrowing costs and persistent inflation pressures, supporting the case for the Fed to keep its benchmark rate at the current 3.50%-3.75% range for an extended period.

The 10-year US Treasury yield climbed alongside the dollar, widening the interest rate differential with Japanese government bonds. Japan’s 10-year yield has risen to around 2.3%, near multidecade highs, as the Bank of Japan signals further policy normalization.

The Bank of Japan held its short-term policy rate steady at 0.75% at its April meeting but indicated a rate hike could come as soon as June.

While the central bank raised its core inflation forecast to 2.8% from 1.9%, it cut its fiscal 2026 growth projection to 0.5% from 1%, reflecting a cautious outlook.

Currency markets remain attentive to intervention risks. Japanese authorities are widely believed to have spent approximately ¥5.4 trillion ($34.5 billion) in late April to support the yen, marking the first such action since July 2024.

Analysts note that early, pre-emptive intervention has lowered the threshold for future official action, though fundamental yield differentials continue to favor the dollar.

Broader geopolitical developments also influenced sentiment. A meeting between US President Donald Trump and Chinese leader Xi Jinping was described as “good,” with both sides discussing enhanced economic cooperation and emphasizing the importance of keeping the Strait of Hormuz open. Meanwhile, elevated oil prices linked to Middle East tensions have contributed to inflation concerns that feed into central bank policy calculations.

Looking ahead, traders are focused on the policy divergence between the Fed and the Bank of Japan. While both central banks are moving toward tighter policy, the pace and magnitude of adjustment differ significantly. The Fed’s cautious stance on rate cuts, paired with the BOJ’s gradual approach to normalization, is likely to keep upward pressure on USD/JPY, though intervention threats may cap sharp moves.

Market participants will monitor upcoming US inflation data and Bank of Japan commentary for further direction. Any sustained break above the 158.40 resistance level could signal a test of the psychologically important 160 level, while a pullback below 157.30 may indicate renewed caution ahead of potential policy shifts or official currency market actions.