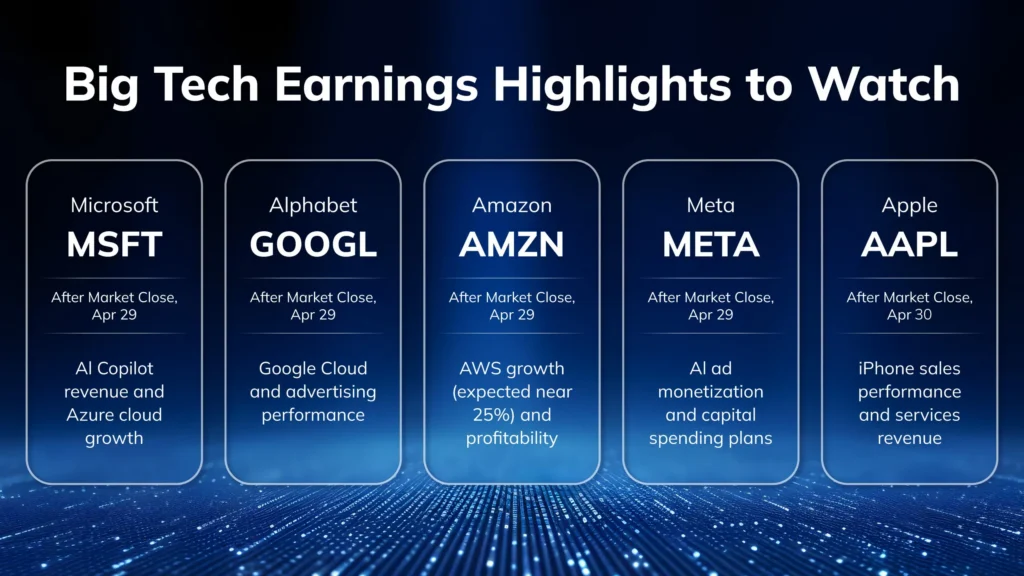

As geopolitical uncertainties continue to loom, the primary stock markets in the United States are approaching a critical inflection point with the impending earnings releases from major technology companies. Alphabet Inc., Microsoft, Amazon, and Meta Platforms Inc. are scheduled to report their financial performance on April 29, followed by Apple Inc. on April 30. Collectively, these firms command an impressive market capitalization of nearly $16 trillion, representing about 25% of the S&P 500 index’s total market cap. This earnings season is poised to exert a significant impact on market sentiment and investor strategies, given the substantial concentration of value among these tech behemoths.

As of April 27, over 25% of S&P 500 companies have reported earnings, and the data indicate a notable increase in both the frequency and magnitude of positive earnings surprises relative to historical norms. According to FactSet, around 84% of these firms have exceeded consensus earnings forecasts. The blended earnings growth rate for the S&P 500 in the current quarter is 15.1%, surpassing the initial projection of 13.2%. Additionally, the anticipated earnings growth rates for 2026 and 2027 are forecasted at 18.6% and 16.1%, respectively, suggesting strong bullish sentiment regarding future corporate performance.

Key Highlights of the 2026 Q1 Earnings Season

- Strong Growth: The blended earnings growth rate for the S&P 500 in Q1 reached 15.1%, marking the sixth consecutive quarter of double-digit year-on-year growth.

- Sector Performance:

- Information Technology leads with an expected growth of 45%

- Materials: +24.2%

- Financials: +15.1%

- Healthcare: -9.8% (decline)

- AI Catalyst: Market focus is centered on AI-driven cloud growth, particularly the AI-related revenues of tech giants like Microsoft, Amazon, and Meta.

- Market Momentum: The S&P 500 has risen nearly 10% since the end of March, on track for its best monthly gain since late 2020. The core driver of this rally is the alignment between optimistic expectations for U.S.-Iran peace talks and the semiconductor sector’s continued strength.

The “Magnificent Seven” are projected to deliver 19% earnings growth in Q1, significantly outpacing the more conservative 12% growth forecast for the broader market. This week’s earnings report is expected to serve as a critical barometer of investor sentiment in the technology sector, particularly amid ongoing geopolitical tensions in Iran, which have been affecting the global economy since late February.

Core Watch Points for Major Tech Earnings

Alphabet (GOOGL): April 29 After-hours

- Google Cloud Growth: Markets expect cloud growth to exceed 50%, driven by enterprise AI adoption and Gemini integration.

- Validation of Capital Expenditure Returns: Alphabet has guided for 2026 CapEx of $175–185 billion, nearly double 2025 levels. Markets are focused on management’s comments on the pace and visibility of returns.

- Search Business AI Defense: Reports need to provide specific data on AI Overview monetization and query volumes to address concerns about AI replacing core search revenue.

Microsoft (MSFT): April 29 After-hours

- Azure Growth: Azure grew 40% year on year last quarter; the focus is on whether there will be an unexpected acceleration this quarter.

- Capital Expenditure: CapEx reached $34.9 billion last quarter; this quarter’s guidance will be a key indicator of the intensity of AI infrastructure investment.

- OpenAI Relationship Dynamics: Recent adjustments to partnership terms and reduced exclusivity have prompted discussions about the sustainability of Microsoft’s AI leadership.

Amazon (AMZN): April 29 After-hours

- AWS Growth as a Decisive Variable: AWS grew 24% year on year to $35.58 billion last quarter, its strongest growth in several quarters.

- Quantitative Validation of AI Business: CEO Andy Jassy disclosed that AWS’s AI business annual revenue run rate has exceeded $15 billion. Markets expect more evidence of AI revenue converting into AWS growth.

- Margin Resilience: With guidance for Q1 operating profit of $16.5–21.5 billion, markets will evaluate if margins can remain resilient amidst massive CapEx.

Meta (META): April 29 After-hours

- Sustainability of Ad Momentum: AI-driven ad efficiency is the core growth driver; Threads is expected to generate $2.7–6.5 billion in revenue in 2026.

- CapEx Pace and Product Updates: Focus is on progress with next-generation AI products such as “Mango” (video and image models), expected in 1H26.

- Cost Control and Margins: Citi believes strong revenue growth will likely offset higher spending pressures.

Apple (AAPL): April 30 After-hours

- Special Background: This report comes amid a leadership transition, Tim Cook will step down as CEO on September 1 to become Executive Chairman, with John Ternus succeeding him.

- iPhone Cycle and Services: Revenue growth may be “strong” (potentially up to 15%), driven by iPhone, Mac, and Services.

- Gross Margin Pressure and Guidance: Rising memory chip costs may pressure margins, but the Q3 revenue guidance upside should offset this.

- AI Strategy and New Hardware: Low expectations for WWDC in June; reports of a foldable iPhone could bring “true new product excitement”.

In-House View: Major technology firms must demonstrate that their substantial capital investments yield measurable returns. Projections indicate that capital expenditures for Microsoft, Alphabet, Amazon, and Meta will escalate to $649 billion in 2026, up from $411 billion in 2025.

Impact of U.S.-Iran Situation on Earnings Performance

The current stalemate in US-Iran negotiations affects the assessment of tech earnings in multiple ways:

- Transmission Effect of Energy Inflation: Current high oil prices can be attributed to the ongoing blockade of the Strait of Hormuz. In April, the U.S. Manufacturing PMI output price index rose substantially to 59.9, the highest level of corporate price increases in 45 months. The escalation in energy costs is undermining purchasing power, which could have downstream effects on corporate IT budgets and consumer demand within the electronics sector.

- Continued Cooling of Rate Cut Expectations: Given the impact of energy inflation, market expectations indicate a mere 26% probability of a rate cut in September, with a slightly higher estimate of 39% for December. The persistence of elevated interest rates continues to exert downward pressure on technology valuations.

Relative Resilience of Tech Stocks: Despite escalating geopolitical risks, the demand for U.S. technology remains resilient compared to other sectors. This resilience can be attributed to the inelasticity of AI investment demand, as well as the substantial pricing power of leading tech firms, exemplified by Microsoft’s ability to implement price increases of 10% to 20%. Additionally, profit margins in the tech sector are less sensitive to oil price fluctuations than those in energy-intensive industries, further underscoring the stability of tech profits in this volatile environment.

Large corporations are increasingly required to demonstrate that their significant financial investments will yield a favorable return on investment (ROI). Projections indicate that the combined capital expenditures of industry giants Microsoft, Alphabet, Amazon, and Meta are expected to rise to $649 billion in 2026, up from $411 billion in 2025. This underscores a substantial increase in projected fiscal commitments as these entities expand their strategic initiatives and operations.

Outlook for U.S. Stocks After Earnings

The S&P 500 and Nasdaq have recently reached new all-time highs. Should the growth trajectory of cloud services among major tech players exceed projections, and if capital expenditure guidance closely mirrors demand, the technology sector could maintain its bullish trend. On the other hand, if there is a cautious outlook regarding energy price pressures or if core business segments underperform, we could see market consolidation or increased apprehension about the ROI of artificial intelligence initiatives.

The Dow Jones Lags Behind: The Dow Jones Industrial Average (DJI) has struggled to maintain momentum amid recent market peaks, capturing little traction from the semiconductor rally. As a price-weighted index, the DJI’s composition is predominantly influenced by the share prices of its highest-priced components, rather than by their market capitalization. Key contributors such as Microsoft and Apple, among the most expensive stocks in the index, have the potential to substantially impact the DJI’s performance. Should their earnings reports exceed market expectations, we can anticipate a significant elevation in the Dow’s overall value.

Conditions for a Dow Rebound Driven by Earnings

| Condition | Impact |

|---|---|

| Microsoft/Apple earnings both exceeded expectations. | Necessary condition; directly pulls the Dow upward. |

| The AI investment narrative is not falsified. | Maintains overall risk appetite. |

| Energy prices do not surge further. | Avoids additional pressure on traditional Dow sectors. |

| Fed resolution does not release extreme hawkish signals. | Avoids offsetting positive earnings. |

Analyst Outlook: If the Dow breaks through the significant 50,000 threshold, the February peak will likely act as the primary target for setting new all-time highs.

Earnings Calendar in May

Week 1: Finance and Growth Stocks (May 4–6)

| Date | Company | Ticker | Focus |

|---|---|---|---|

| May 4 (Mon) | Palantir | PLTR | AI data analysis leader, enterprise customer growth rate |

| May 4 (Mon) | PINS | Social media ad revenue, user conversion rate | |

| May 5 (Tue) | PayPal | PYPL | Payments leader, margin improvement, buyback plan |

| May 5 (Tue) | AMD | AMD | AI chip (MI300/MI400 series) sales progress |

| May 5 (Tue) | Pfizer | PFE | Pharmaceutical business performance |

| May 5 (Tue) | Shopify | SHOP | E-commerce platform growth |

| May 5 (Tue) | Super Micro | SMCI | AI server demand |

| May 6 (Wed) | Disney | DIS | Streaming profitability, theme park revenue |

| May 6 (Wed) | Uber | UBER | Delivery and ride-sharing business profit margins |

| May 6 (Wed) | Kraft Heinz | KHC | Food consumer products performance |

| May 6 (Wed) | Arm Holdings | ARM | Chip IP licensing and AI-related business |

Mid-Month: Retail Giant Week

| Date | Company | Ticker | Focus |

|---|---|---|---|

| Approx. May 14 | Walmart | WMT | E-commerce growth, grocery market share |

| Approx. May 20 | Target | TGT | Recovery of discretionary consumer spending |

Late-Month: Ultimate AI Bellwethers

| Date | Company | Ticker | Focus |

|---|---|---|---|

| Approx. May 20/27 | NVIDIA | NVDA | Q1 revenue, Blackwell chip supply/demand and guidance |

| Approx. May 21 | Applied Materials | AMAT | Semiconductor equipment market |

The performance of the retail sector will serve as a key indicator for assessing scenarios for a “soft landing” in the economy. At the same time, the industrial semiconductor sector is experiencing significant growth, heralding a new “super cycle.” This upturn is fueled by increasing demand that extends well beyond just artificial intelligence applications.

Disclaimer: The views, scenario-based deductions, and market judgments presented in this article are for reference and communication purposes only and do not constitute any form of investment advice, buying or selling recommendations, or recommendations for any financial products.